提高盈利的五个方法

我们必须把12%的资本回报率看成是不变的吗?有没有一条法律规定:公司资本回报率不能自我调节,来应对长期的更高的平均通货膨胀率?

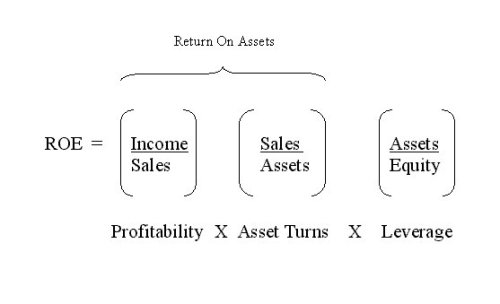

当然,并没有这样一条法律。恰恰相反,美国企业无法通过意愿或者命令增加盈利。为了提高资本回报率,企业需要至少下面的其中一项:

1)提高周转率,也就是销售额与总资产的比。

2)廉价的债务杠杆

3)更高的债务杠杆

4)更低的所得税

5)更高的运营利润率

这就是所有的方式。根本没有提高普通股资本回报率的其他方式。让我们看看我们如何利用这些方式。

我们先从周转率开始。为了分析周转率,我们必须考虑三个主要类型的资产:应收帐款、库存和固定资产,如厂房和机器。

应收帐款随销售额增加成比例增加。而以美元计的销售额增加是由销量增加或通货膨胀引起。在这里没有改善的空间。

库存的情况非常不简单。从长期看,计件的实体库存数量趋势跟随销量趋势。但是从短期看,实体库存的周转率会上下波动,原因可能是空间影响、成本预期、或者生产瓶颈。

在通胀时期,使用后进先出库存估值方法会提高报告的周转率。当由于通货膨胀引起销售额上升,使用后进先出方式的公司库存值要么会保持不变(如果销量不增加),要么会跟随销售额上升(如果销量上升)。无论哪种情况,以美元计的周转率都会提高。

在70年代早期,公司的一个显著趋势就是转向“后进先出”会计方式(这样做有降低公司报告的盈利和降低税的效果)。这一趋势目前似乎有所减缓。但是,很多“后进先出”公司的存在,加上很多其他公司也可能加入“后进先出”这一行列,会使未来报告的库存周转率提高。

Five ways to improve earnings

Must we really view that 12 percent equity coupon as immutable? Is there any law that says the corporate return on equity capital cannot adjust itself upward in response to a permanently higher average rate of inflation?

There is no such law, of course. On the other hand, corporate America cannot increase earnings by desire or decree. To raise that return on equity, corporations would need at least one of the following: (1) an increase in turnover, i.e., in the ratio between sales and total assets employed in the business; (2) cheaper leverage; (3) more leverage; (4) lower income taxes, (5) wider operating margins on sales.

And that's it. There simply are no other ways to increase returns on common equity. Let's see what can be done with these.

We'll begin with turnover. The three major categories of assets we have to think about for this exercise are accounts receivable inventories, and fixed assets such as plants and machinery.

Accounts receivable go up proportionally as sales go up, whether the increase in dollar sales is produced by more physical volume or by inflation. No room for improvement here.

With inventories, the situation is not quite as simple. Over the long term, the trend in unit inventories may be expected to follow the trend in unit sales. Over the short term, however, the physical turnover rate may bob around because of special influences - e.g., cost expectations, or bottlenecks.

The use of last-in, first-out (LIFO) inventory-valuation methods serves to increase the reported turnover rate during inflationary times. When dollar sales are rising because of inflation, inventory valuations of a LIFO company either will remain level, (if unit sales are not rising) or will trail the rise in dollar sales (if unit sales are rising). In either case, dollar turnover will increase.

During the early 1970's, there was a pronounced swing by corporations toward LIFO accounting (which has the effect of lowering a company's reported earnings and tax bills). The trend now seems to have slowed. Still, the existence of a lot of LIFO companies, plus the likelihood that some others will join the crowd, ensures some further increase it the reported turnover of inventory.

0

推荐

京公网安备 11010502034662号

京公网安备 11010502034662号 {kind=link}